I wrote the following paper for my coursework in EME 7634: Advanced Instructional Design, instructed by Dr. Atsusi Hirumi. Net-worth calculation was my chosen topic, due to my persistent interest in financial education.

I am also making this paper and companion slides available for download. The companion slides are not included in the paper. They were made two weeks before I wrote this paper, prior to conducting the actual task analyses.

Download paper as Microsoft Word 2016 document

Download paper as PDF

Download companion slides as Microsoft PowerPoint 2016 file

Download companion slides as PDF

My work should only be used appropriately and I should be credited.

Task Analysis Comparison for Calculation of Net Worth

Richard Thripp

University of Central Florida

March 1, 2017

Calculating one’s net worth is a vital part of financial literacy (French & McKillop, 2016). Tallying the value of one’s assets and debts improves understanding of one’s financial situation. Although at first, this process may seem simple, appraising one’s assets is a complex issue, and even remembering all of one’s possessions and liabilities may be difficult. Therefore, net-worth calculation seems a suitable instructional situation to analyze. For this portfolio analysis, I am applying three alternative analysis techniques that were included in Jonassen, Tessmer, and Hannum’s (1999) handbook—procedural analysis, critical-incident analysis, and case-based reasoning (CBR). The former two are differentiated by their focus on overt elements and underlying methods, respectively, while CBR’s status as a task-analysis method is tenuous and its utility in this situation is marginal—it is included here for demonstration purposes.

Procedural Analysis

This type of analysis is geared toward assembly lines and other easily observable tasks. However, it can be used to describe cognitive activities if they are overtly observable, and when extended with flowcharting, can even describe relatively complex decision-making processes.

The following analysis is for the net-worth calculation task, based on the steps described by Jonassen et al. (1999, pp. 47–49):

- Determine if the task is amenable to a procedural analysis. Listing assets and liabilities, looking up their values, and sometimes, appraising values are overt actions and can be conceived as a series of steps. However, recalling all relevant items and appraising values can require covert cognitive processes in some cases, so procedural analysis does not capture everything required for this task.

- Write down the terminal objective of the task. “Calculates their net worth by estimating and tallying the values of their real assets and liabilities.” Note that this task excludes analyses of liquidity, cash flow, monthly expenses, and interest rates on debts, which are also important components of one’s financial situation.

- Choose a task performer. I am the performer for this task. I achieved competence in this task three years ago. If the training is for novices, Jonassen et al. (1999) say the flowchart should be based on someone who has only achieved expertise recently, to avoid “an idiosyncratic sequence” (p. 47). For this task, Investopedia’s Net Worth Calculator (www.investopedia.com/net-worth) was examined to help guide the analysis. Additionally, based on my knowledge of personal finance, I accounted for a variety of common financial situations (e.g., marriage, retirement funds, etc.).

- Choose a data-gathering procedure. I took notes as a silently executed the task.

- Observe and record the procedure. I made a text-based list of tasks before starting, and opted to construct a flowchart while executing the net-worth task.

- Review and revise outline. This step was skipped, because I did not do an outline.

- Sketch out a flowchart of the task operations and decisions. See Figure 1. In constructing this flowchart, is was readily apparent that a complete flowchart would be “cumbersome in detail” (Jonassen et al., 1999, p. 53). Consequently, I constructed the flowchart at an abstracted level that condenses or generalizes many steps. For example, Item 210: “Cash equivalent asset or debt?” actually applies to a host of items including bank accounts, taxable investment accounts, mortgages, student and auto loans, and credit card debts. Item 120: “Recall and list real assets and liabilities …” implies the learner will list assets and debts as separate line items (e.g., house and mortgage would be listed separately). These details and others are omitted from the flowchart to prevent it from becoming overwhelming and unwieldy. At Item 200, a foreach loop is used to iterate over the array (list) of assets and debts, similar to the foreach construct in PHP, a popular web scripting language.

- Review the procedural flowchart. This was done during its construction.

- Field-test the flowchart. I compared the flowchart to the Investopedia’s Net Worth Calculator (www.investopedia.com/net-worth) to see if it could fit the same situations. The categories of assets and liabilities on this calculator all fit into items on the flowchart. A net-worth spreadsheet is more versatile than Investopedia’s calculator because it can be saved, amended, and reused.

Figure 1. Procedural-analysis flowchart for net-worth calculation task.

Critical-Incident Analysis

This type of analysis involves interviewing subject-matter experts (SMEs) to gain a realistic understanding of the task at hand, including the important elements (Jonassen et al., 1999). Interview or survey data from SMEs must be culled to remove noncritical elements, focus on the required behavior, and to arrange tasks by importance (Flanagan, 1954). You can also ask your SMEs to arrange tasks by importance (Jonassen et al., 1999).

As compared to procedural analysis, critical-incident analysis may capture realistic information that is not elucidated in a procedural analysis, including antecedents and prerequisites, considerations for subjective decisions, and other “covert” elements that are not outwardly observable (Jonassen et al., 1999).

Interview

For this critical-incident analysis, I interviewed myself using a variation of Flanagan’s (1954) sample interview form from Jonassen et al. (1999, p. 184), which was modified to fit the net-worth calculation task:

- Describe an incident that you remember which was an example of effective net-worth calculation. A friend of mine was looking to apply for a mortgage and pay a 20% down payment on a house. She was adept at personal finance and had only minor debts. She calculated her net worth and liquidity (available cash) to get an up-to-date picture of her financial state and determine her price ceiling while house hunting, considering her state of liquidity. While a net-worth calculation was just part of many things she did, it was important nonetheless.

- What were the general circumstances leading up to this incident? She wanted to move to a different part of the country, away from her parents, and buy a house of her own. She already owned a house locally that she was renting out. While this friend used strategies to increase her liquidity that I would not recommend, such as leveraging 0% promotional APR periods on credit cards to buy cash equivalents to convert to cash, she timed it in such a way that the increased credit utilization did not downwardly influence the credit scores reported by credit bureaus for her mortgage applications.

- Tell me exactly what this person did that was so effective at the time. In her net-worth calculation, she was conservative because she did not want to overestimate her net worth. Even though she might have been able to sell her car for $5000, she put $3500 in her spreadsheet to err on the side of caution. She decided not to include the house she already owned in her spreadsheet, since she had no intention of selling it and did not want an overly rosy picture of her situation. However, she did include the monthly expenses and rent income in a separate spreadsheet to calculate her monthly cashflow, and it was very smart that she looked for a mortgage payment that was less than 40% of her net income. Further, she did not include personal possessions in her net worth because she did not considering selling them to be a realistic scenario.

- How did this incident contribute to the individual’s overall financial situation? She decided to be somewhat more conservative with the house she intended to purchase, to not overly extend herself financially. In the event of job loss or a recession, this could be the difference between scraping by and being foreclosed on.

Analysis

This critical-incident analysis is based on the above interview, using the steps described by Jonassen et al. (1999, pp. 183–185):

1. Gather the incidents. For this analysis, only the above incident was considered.

2. Condense incidents into statements of behavior. The incident included extraneous details about cashflow, liquidity, credit, and a home search, which are not directly related to a net-worth calculation. Also, the details on net-worth calculation were not specific enough to yield specific steps as to how to conduct the process. SMEs often fail to sufficiently describe a process or break it down into the relevant steps. As suggested by Jonassen et al. (1999), I have condensed the interview into these statements about behavior relating to net-worth calculations:

• 2.1. The estimated value of assets should be conservative if one wants a cautious estimate of their net worth.

• 2.2. One can choose not to include an owned home if they have no intention of liquidating the asset and do not want to consider it in their net-worth estimate.

• 2.3. One can choose to omit low-value or personal items to simplify calculations and exclude items which would not be easily sold.

• 2.4. One’s net worth is an important metric, but many others are important too. A good net-worth spreadsheet might actually be constructed with separate sections for liquid and illiquid assets. Also, it should be augmented with a cashflow spreadsheet detailing one’s monthly expenses and incomes.

3. Test for statements for criticality. Statements 2.1–2.3 can be condensed into this general statement:

• 2.1–2.3. One chooses which assets to consider and how to appraise them. While financial accounts and debts may be simple, illiquid, harder-to-sell assets might be appraised conservatively if one wants a cautious analysis. Personal items may be omitted for simplicity, and due to their low resale value.

I also believe it is critical to add the following statements:

• 2.5. Recalling all debts and including their balances is important for an accurate net-worth spreadsheet. Primarily, debts include a mortgage, auto loan, student loans, and credit cards.

• 2.6. For most purposes, a conservative net-worth estimate is probably better than a liberal estimate. One can always find a use for more money, but believing one has more net worth than they do may result in poor decisions (Lusardi & Mitchell, 2007).

• 2.7. Calculation of net-worth is more complicated if one owns a business or has joint finances (e.g., marriage). One must decide in how to handle such arrangements.

4. Organize or arrange the competency statements. As recommended by Flanagan (1954), I arranged the statements from least to most important as follows:

• Least important: 2.7: Deciding how to handle businesses or joint finances (e.g., marriage) is probably beyond the scope of the net-worth calculation task.

• 2.6: While this may be good advice, it is not directly related to the task.

• 2.4: This is somewhat more important because it recommends separating liquid and illiquid assets, which is something that was not elucidated in the procedural analysis. Also, it notes the limitations of net-worth calculations, which may have tangential behavioral implications.

• 2.5: Recalling all debts is a critical part of net-worth calculation. In particular, individuals who lack financial literacy may be surprised to find they have a lower-than-expected or negative net worth (van Rooij, Lusardi, & Alessie, 2012). If debts are forgotten, one’s net-worth calculation will be rosier than reality.

• Most important: 2.1–2.3: These decisions are a vital and subjective part of net-worth calculations that are difficult or impossible to express in a procedural analysis.

Distillation

Jonassen et al. (1999) recommends distilling the incidents and grouping them into effective and ineffective categories. While my critical-incident analysis did not consider ineffective incidents, I covered them below by extrapolation.

- Effective: Deciding the purpose of the net-worth calculation and being appropriately conservative in inclusion and appraisal of assets.

- Effective: Doing separate calculations for liquid and illiquid net-worth and perhaps producing two figures, one including all assets, and one including only assets that are easily liquidated.

- Effective: Recalling and including all debts and the amounts owed, such as a mortgage, auto loan, student loans, and credit cards.

- Ineffective (extrapolated): Including personal items valued at their purchase price. If purchased at full retail, electronics and furniture may easily lose half their value or even more when attempted to be resold. Similarly, automobiles depreciate precipitously.

- Ineffective (extrapolated): Conducting a net-worth calculation in lieu of other processes such as budgeting, credit score optimization, a cost-of-debt-service analysis, and an income analysis. Net worth is just one piece of the puzzle.

Case-Based Reasoning

CBR is not commonly used as an analysis technique. However, Jonassen et al. (1999) have included it on the basis that “knowledge engineers [who] design intelligent systems” (p. 148) employ CBR as a task-analysis method. Although using it for the task of net-worth calculation is tenuous, it is included here for demonstration purposes.

Jonassen et al. (1999) recommend using a database management system to gather and catalog cases along many indices including motives expressed in the case, solutions employed, and resultant outcomes. Without much evidence, they suggest such a database can be leveraged to provide effective case-based instruction, and predict this will become common in the future.

For this analysis, I selected two cases and two anecdotes from anonymous commentators on an online, publicly viewable bulletin board (www.early-retirement.org/forums/f28/very-small-networth-when-er-84557.html), and included a sample net-worth spreadsheet from the net-worth video module in my Introduction to American Personal Financial Literacy online course (http://thripp.org/fin-lit-intro/). Then, I discussed the implications of these cases and anecdotes.

Anecdotes and Cases

Figure 2. Anecdote 1. Bulletin board post by “Bir48die,” December 13, 2016.

Figure 3. Anecdote 2. Bulletin board post by “marko,” December 13, 2016.

Figure 4. Case 1. Bulletin board post by “FUEGO,” December 13, 2016.

Figure 5. Case 2. Bulletin board post by “pmac,” December 13, 2016.

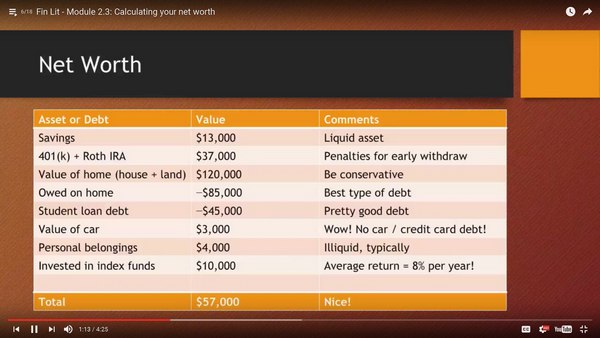

Figure 6. Case 3. From my Introduction to American Personal Financial Literacy online course.

Discussion and Analysis

From the anecdotes (Figures 2–3), we see there are many facets to net-worth calculations. Because this discussion was on a bulletin board focused on early retirement, some items do not apply to the task at hand, but nevertheless help us see the bigger picture. Our procedural and critical-incident analyses did not directly reveal anything about cost of living, age, pensions, or other variables. Strictly speaking, these are not even parts of a net-worth calculation, yet are arguably just as important to assessing one’s financial situation.

In Cases 1–2 (Figures 4–5), we see that both commentators are married millionaires who and about to retire or recently retired. Both “pmac” and “FUEGO” discuss or allude to net worth being a fairly limited figure that does not consider a host of other factors. “FUEGO” is unusual, having “retired” a millionaire at Age 33 with a wife and three children. His story elucidates a peculiar property of net worth: even as a millionaire, due to having low income, his family is eligible for Medicaid and perhaps other need-based aid that does not account for accumulated assets. We also see two different perspectives on net-worth calculation: “pmac” advocates a very conservative approach, at least for the purpose of deciding whether early retirement is an option. His approach includes savings and investments with an upward adjustment for anticipated retirement benefits, but omitting the value of one’s primary residence, automobiles, and other illiquid or depreciating assets. On the other hand, “FUEGO” thinks it is perfectly fine to include his primary residence’s value in his calculation. These insights illuminate factors and decisions in net-worth calculation that were not revealed in procedural and critical-incident analyses.

Case 3 (Figure 6) is a contrived teaching tool complete with comments that may be of use to the novice learner. A key assumption of our procedural flowchart was that the learner would be calculating assets and debts, even if owed on the same asset, as separate line items. This case shows such formatting in action—the mortgage is listed separately from the home’s value. If an auto loan would be included, it would be listed separately from the vehicle’s value as well. The instructor’s comments increase this case’s value as a teaching tool, such as comments about liquidity and the merit of various types of debt. However, it should be noted that recent research and position papers have argued against the traditional conception that mortgages and student loans are praiseworthy forms of debt (e.g., Ross & Squires, 2011; Doran, Kraha, Marks, Ameen, & El-Ghoroury, 2016). Jonassen et al. (1999) recognize that a major limitation of CBR is that instructors may reuse old cases even when they are no longer applicable or valid. Further, CBR may not provide the level of instruction or scaffolding that novices may require (Kirschner, Sweller, & Clark, 2006; van de Pol, Volman, & Beishuizen, 2010). Therefore, I do not contend that CBR should be an appropriate primary teaching method for novices, which is the intended target group for this task-analysis. Moreover, CBR is not actually a task-analysis method.

Overall Reflection

Looking at these three methods shows us three fairly different ways to look at the net-worth calculation task. I found the procedural analysis to be the most challenging and useful. Laying out the flowchart gave me a greater appreciation for the underlying complexity of this seemingly simple task. I was acutely aware that I was condensing or glossing over many steps when constructing figures in the flowchart, and yet had I not done this, the flowchart would have been of an overwhelming size and complexity. It would also have required many additional hours of work. However, this flowchart seems somewhat disconnected from actual financial practice and does not adequately represent subjective and hidden issues. It seems that critical-incident analysis did a better job of representing these details, albeit with a lack of procedural rigor, although that was partly due to not interviewing multiple experts.

The procedural analysis’s focus on overt behaviors is a major limitation. For the net-worth calculation task, critical-incident analysis revealed the importance of liquidity and the subjectivity of judgments about what assets to include in the net-worth spreadsheet and how conservatively to appraise them. While I hinted at these subjective elements in the notes relating to the procedural-analysis flowchart, it would have been too onerous to accurately represent them within the flowchart. For this task, it seems that both analyses were valuable in their own way, and in fact, it is not unheard of to augment procedural analysis—Foshay (1983) recommends following up with a learning-hierarchy analysis.

CBR, while not suited to task analysis, may better capture the interests and attention of learners. However, there are many shortcomings. Novices could easily select the wrong case—for instance, an apartment-dweller without a car in New York City is going to have a very different net-worth spreadsheet from a suburban automobile-commuter who owns a single-family home. Potentially, case-based instruction may exhibit an expertise reversal effect (Kalyuga, 2007) whereby experts learn better from cases while novices are bewildered. Although this is pure speculation on my part, it was apparent that the commentators on the Early-Retirement bulletin board considered many fringe issues that were not revealed in my other analyses. Addressing these issues may overwhelm novices who have not yet learned the basics of calculating one’s net worth, yet entice and extend the knowledge of intermediate and expert learners. Through this argument, I contend that CBR has its place if the goal is to “preach to the choir,” so to speak—that is, to help learners who are already well-versed and proficient in net-worth calculations to extend their understanding—but, because my goal was to teach novices, procedural and critical-incident analyses were more appropriate here.

References

Doran, J. M., Kraha, A., Marks, L. R., Ameen, E. J., & El-Ghoroury, N. H. (2016). Graduate debt in psychology: A quantitative analysis. Training and Education in Professional Psychology, 10, 3–13. http://doi.org/10.1037/tep0000112

Flanagan, J. C. (1954). The critical incident technique. Psychological Bulletin, 51, 327–358. http://doi.org/10.1037/h0061470

Foshay, W. R. (1983). Alternative methods of task analysis: A comparison of three techniques. Journal of Instructional Development, 6(4), 2–9.

French, D., & McKillop, D. (2016). Financial literacy and over-indebtedness in low-income households. International Review of Financial Analysis, 48, 1–11. http://doi.org/10.1016/j.irfa.2016.08.004

Jonassen, D. H., Tessmer, M., & Hannum, W. H. (1999). Task analysis methods for instructional design. Mahwah, NJ: Lawrence Erlbaum Associates.

Kalyuga, S. (2007). Expertise reversal effect and its implications for learner-tailored instruction. Educational Psychology Review, 19, 509–539. http://doi.org/10.1007/s10648-007-9054-3

Kirschner, P. A., Sweller, J., & Clark, R. E. (2006). Why minimal guidance during instruction does not work: An analysis of the failure of constructivist, discovery, problem-based, experiential, and inquiry-based teaching. Educational Psychologist, 41, 75–86. http://doi.org/10.1207/s15326985ep4102_1

Lusardi, A., & Mitchell, O. S. (2007). Baby Boomer retirement security: The roles of planning, financial literacy, and housing wealth. Journal of Monetary Economics, 54, 205–224. http://doi.org/10.1016/j.jmoneco.2006.12.001

Ross, L. M., & Squires, G. D. (2011). The personal costs of subprime lending and the foreclosure crisis: A matter of trust, insecurity, and institutional deception. Social Science Quarterly, 92, 140–163. http://doi.org/10.1111/j.1540-6237.2011.00761.x

van de Pol, J., Volman, M., & Beishuizen, J. (2010). Scaffolding in teacher–student interaction: A decade of research. Educational Psychology Review, 22, 271–296. http://doi.org/10.1007/s10648-010-9127-6

van Rooij, M. C. J., Lusardi, A., & Alessie, R. J. M. (2012). Financial literacy, retirement planning and household wealth. The Economic Journal, 122, 449–478. http://doi.org/10.1111/j.1468-0297.2012.02501.x